In 2018, Hipgnosis is the future. The music management group has launched a royalty fund in London with a complex corporate structure and an asset class that might be considered cool, at least relative to peers.Founder and manager Merck Mercuriadis appears in places not typically associated with closed-end investment trusts, such as billboard magazine and background MTV Music Awards.

Collection of hundreds of directories Press release The Hipgnosis Songs Fund may then be liquidated.

HSF shareholders will vote later this month on whether to continue holding the fund, which tends to trade at a discount of about 50% to its published net asset value.It turns out that cool asset classes involve esoteric valuation methods, and income funds are very sensitive to factors like interest rates and cash flow visibility; see Alpha City Passim.

HSF shareholders have been pushing for incentives to vote for another five years, worried about whether The Chainsmokers and Shawn Mendes have the staying power. Today, they got one: a stock buyback plan of up to $180 million and lower advisory fees from Hipgnosis Song Management, the investment adviser formerly known as The Family that actually employs the Mercuridas family.

There is something special about this proposal.

HSF funded the cash return by selling 19% of its portfolio to Blackstone for $465 million, a related-party transaction. Blackstone acquired a majority stake in Hipgnosis Song Management for undisclosed terms in 2021, committing $1 billion to Mercuriadis so he could Establish your own private equity fund.

Shareholders of the public company accepted this at the time, hoping that Blackstone’s involvement would add some professionalism to operations, despite the apparent conflict it created. They have been invited nine times since the IPO and recently received a commitment from HSF that they would not raise further acquisition capital for at least a year.

The suspicion is that Mercuriadis is looking for a different outlet for his hoarding tendencies. Blackstone built a private portfolio that included songbooks from music festival guests including Justin Bieber, Nelly Furtado and HSF co-founder Nile Rodgers, while the publicly traded fund struggled. Whatever professionalism this relationship encouraged within Hipgnosis is not evident in Hipgnosis. share price.

In today’s deal, Blackstone-owned funds will buy some songs from HSF. The catalog to be disposed of (known as the first sets) is on average slightly newer than the retained sets, which will increase its proportion of “culturally important and successful songs,” according to a statement from the HSF. The explainer also mentioned that without a manager change, the artists should remain happy – although being placed in a culturally unimportant deal group may not help matters with the likes of Barry Manilow and Kaizer Chiefs relation.

HSF said it had “established appropriate governance arrangements and information barriers” between Hipgnosis (PLC), Hipgnosis (Blackstone) and Hipgnosis (the management group). Liberum Capital calls this a “boilerplate statement”:

We believe these are standard measures of good governance, but it leaves us with the question of where the really good investment team members will sit within an investment advisor. Will they join the team advising the company, or will they join the team advising Hipgnosis Song Capital (owned by Blackstone)? Additionally, will two teams of investment advisors use the same model to evaluate the catalog? If so, it wouldn’t surprise anyone that even if the Chinese Wall existed, the two teams would have similar ideas and not be independent when assessing the value of the catalog.

Wouldn’t it be cleaner to sell Blackstone a simple percentage share of the entire song collection? Are the above assets better or worse than the portfolio average?Do new rules Author: Dua Lipa and Yes! DCF by Usher (both in disposition group) better or worse than at all costs by imaginary dragon or Offal! by System of a Down (both retained by HSF)?

who knows? Who might know?

“The main objective of this transaction is to get NAV comfort and re-rate the share price. The complexity of the deal shows that it is difficult to say that the NAV has been validated,” Stifel analyst Sachin Saggar wrote. “Perhaps this is consistent with our skepticism of valuation agencies.”

HSF outsourced the catalog evaluation to Massarsky Consulting, owned by Citrin Cooperman since 2022. In May 2022, Citrin Cooperman’s Nari Matsuura gave a great interview to Music Business Worldwide about “When interest rates rise, we won’t have to increase the discount rate,” and “How we protect all our customers: Valuations won’t go down. ” When an independent evaluator says something like this, some skepticism may be warranted.

The song collections were sold at a discount of 17.5% to the fair value given on March 31, 2023. That’s a bit strange, not least because it compares quite poorly to HSF’s only peer on the London market, Round Hill, which last week received a privatization offer at an 11.5% discount to net asset value. Additionally, this is an overall discount as it does not take into account bonuses, bonuses and other contingent payments, which will be paid by HSF rather than Blackstone, subject to a cap of $30 million.this actual Discounts may be in the low to mid 20% range.

Valuation must also consider aggregate and fundamental levels. Blackstone has agreed to pay 18.3 times the catalog’s historical net publisher share, which is quite high by industry standards for a B-rated portfolio, but royalties, etc., are retroactive to the beginning of the year. There is already $15.3 million in arrears accrued, so if the deal closes before the end of the year, the purchase price will fall by about 5%.

Unusually for a UK deal, there is a “go-shop” clause which gives other interested parties 40 days to come up with a better proposal. But they must pay a $6.6 million break fee to management company Hipgnosis Songs Capital and take into account the dead-end risk that their offer will be matched. As the fine print says:

If Hipgnosis Songs Capital matches the Superior Proposal, the transaction will be final and binding and the Company will not engage in any further discussions or negotiations with any person regarding the Superior Proposal or other alternative transactions.

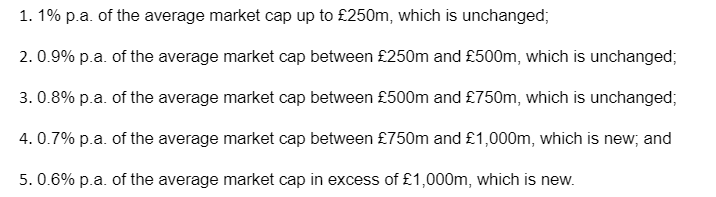

Among other sweeteners, HSF’s revolving credit facility pays out $250 million to address interest costs, which have reached extremely high levels in recent years for obvious reasons, and Reduce management fees If the market cap stays around current levels. The fee concession exposed possible conflicts of interest within the group, Liberum explained:

Does the investment advisor end up making more money from managing the first portfolio in-house at Hipgnosis Songs Capital than the lost revenue from (HSF) investment advisory fees? If so, what impact will these incentives have on the proposed transaction? What incentives are there for Merck Mercuriadis after the deal? We do not intend to accuse investment advisers of cherry-picking or manipulating dispositions for their own benefit, but we would like to see more transparency in the deal and the incentive structure for all parties involved.

Overall, we can’t shake the impression that the company has received a lot of feedback from investors that a continued vote might fail, and last week’s announcement by the Round Hill Music Royal Fund to sell its entire portfolio may force the board to sell some products. Family money. Whether this calms investors, we believe, will largely depend on reassuring them that the book NAV of the remaining portfolios has not been inflated, that governance issues are properly addressed and that incentives are truly aligned with shareholders for investment advisers to provide The best service is from this company and not Hipgnosis Songs Capital.

Stifel provides a more succinct summary:

It’s unclear how shareholders will assess whether the deal is a good or bad one, given the structure involved, which could be a hurdle.

Ultimately the Blackstone acquisition was the only clean solution for shareholders, so although entirely hypothetical, it became an important part of the HSF investment case. Of course, Blackstone’s funds are also the most likely buyers of liquidated assets and have just set a lower valuation benchmark.

Ahead of the AGM vote, Mercuridas gave shareholders another chance to get their hopes up for five years, but also made clear again why his company is not suitable for public markets.

Winterflood Securities said: “We would not be surprised to see a relatively small margin in votes.” Ibid.

Further reading:

— Yield-obsessed investors shouldn’t put too much faith in Hipgnosis (FT, 2020)

— Stifel Worries Hipgnosis Song Fund Is Going Out of Tune (2021)

— The music continues to play at Hipgnosis (FTAV, 2021)

Svlook

{kind=link}